Division 296 Super Tax

13th March 2026: Key changes to the Division 296 law have passed the Senate and received royal assent.

Division 296 isn’t a 30% tax on your super — it’s an additional tax on a portion of earnings for balances above $3 million.

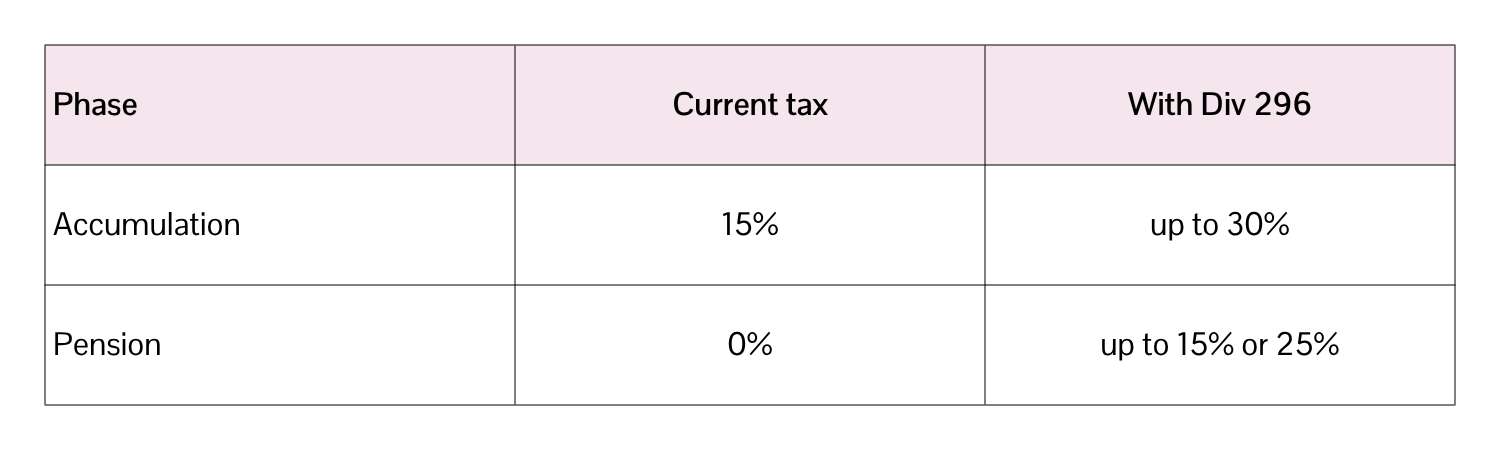

Firstly, let’s recap the current tax that applies to Super earnings: 15% for Accumulation phase accounts and 0% for Pension phase accounts. Here are five important points:

1. Start date confirmed

The tax commences 1 July 2026, with the first assessment based on balances and earnings for FY2026-27 (i.e. assessed after 30 June 2027).

2. Only realised earnings are taxed

The most controversial feature — taxing unrealised gains — was removed from the final legislation.

Division 296 applies only to taxable / realised super earnings, such as:

dividends and distributions

interest

realised capital gains

Unrealised market value movements are not included

3. Two-tier tax structure confirmed

The additional tax is:

15% extra tax on earnings attributable to balances above $3m

25% total extra tax on earnings attributable to balances above $10m

When combined with existing tax rates, this results in:

4. Balance calculation change

From 2027-28 onward, the proportion above $3m will be calculated using the higher of the start-of-year or end-of-year balance.

However:

Special transitional rule for FY2026-27: Only the 30 June 2027 balance is used.

5. Transitional CGT reset allowed

Funds may elect to reset asset cost bases to market value on 30 June 2026 so that gains accrued before the new tax starts are not taxed under Division 296.

Here are some important things to remember, and what we’ll be considering in our advice:

Division 296 is calculated on the Total Super Balance

The ATO aggregates everything, so:

✔ multiple funds don’t matter

✔ pension vs super phase doesn’t matter

✔ SMSF vs industry fund doesn’t matter

What happens when a spouse inherits super:

Because the tax is calculated on the Total Super Balance, when inheriting a spouse’s Super or Pension, it can increase the balance suddenly. Some strategies we can consider:

1 - Death benefit withdrawals

Sometimes it may be tax-efficient to withdraw part of the death benefit from super rather than retain it all inside super.

2 - Equalising super balances earlier

Some advisers are now recommending earlier balance equalisation between spouses so that one death does not suddenly push the survivor into very large Division 296 exposure

3 - Asset location and Tax Aware Portfolio strategies

The tax is calculated proportionally, so trying to quarantine high-income assets in balances below $3m won’t work. The ATO effectively assumes all assets produce earnings proportionately.

So, although asset allocation strategies don’t avoid the Div 293 Tax, they still matter for overall tax efficiency. Example strategies that could still work:

managing realised capital gains

holding longer-term assets in super

tax-efficient distribution funds

controlling turnover

Which brings us to the biggest challenge we can see for clients with balances over $3m…

Industry Super Funds – pooled investments

Most industry super funds operate primarily as pooled investment structures, although some also offer limited member-directed options.

Large, pooled funds often hold:

infrastructure

private equity

unlisted assets

internal trading strategies

When those assets are sold or revalued, large, realised gains can occur. Members with balances above $3m cannot control this timing. This is important for Division 296 planning, because realised gains may occur even if the member did not sell anything personally.

Planning Opportunities

The Government believes that about 8,000 Australians will be affected by this new tax. However, the flow-on effects could be felt across many more accounts and effect more people than intended.

The timing of realised earnings inside super matters more than before. And seeking (good) financial advice, matters more than ever.

General Advice Warning

The information in this presentation and the links has been prepared for general information purposes only and does not consider your personal objectives, financial situation or needs. It is not intended to provide commercial, financial, investment, accounting, tax or legal advice. You should, before you make any decision regarding any information, strategies, or products mentioned in this email, consult a professional financial adviser to consider whether it is suitable and appropriate for you and your personal needs and circumstances. Before deciding to acquire a financial product, you should obtain and read the Product Disclosure Statement (PDS) relating to that product, together with the Target Market Determination (TMD).

Antoinette Mullins

GradDipFinPlan| CFP® | B.Diac | ADFS (FP) Certified Financial Planner® & Director

Antoinette Mullins is an Authorised Representative (No. 316376) of Spark Advisors Australia Pty Ltd

Tanya Oddo

BA-BCom|DFP

Financial Planner & Director

Tanya Oddo is an Authorised Representative (No. 284500) of Spark Advisors Australia Pty Ltd

ABN 34 122 486 935 AFSL 380552